All Categories

Featured

Table of Contents

Simply like any kind of various other irreversible life policy, you'll pay a normal costs for a last expenditure policy in exchange for an agreed-upon survivor benefit at the end of your life. Each carrier has different regulations and options, yet it's reasonably easy to handle as your recipients will have a clear understanding of how to spend the cash.

You might not need this sort of life insurance policy. If you have irreversible life insurance in position your last costs might already be covered. And, if you have a term life policy, you may be able to transform it to an irreversible plan without several of the extra steps of getting last expense coverage.

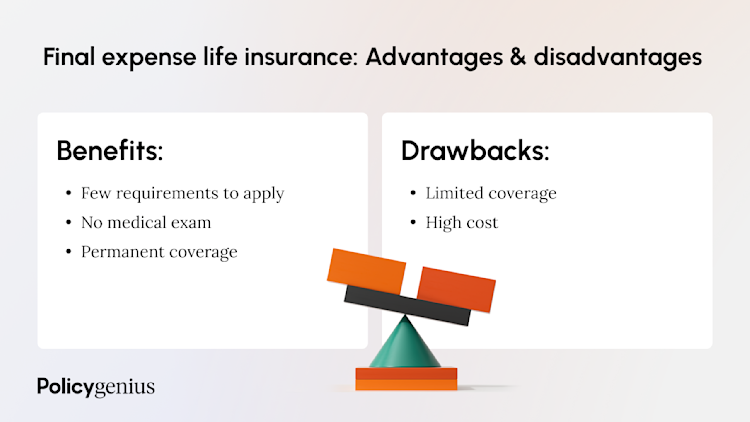

Developed to cover minimal insurance needs, this type of insurance policy can be a budget-friendly option for people who simply desire to cover funeral prices. (UL) insurance continues to be in place for your entire life, so long as you pay your premiums.

About Burial Insurance

This alternative to last expenditure protection gives options for extra family members protection when you require it and a smaller coverage amount when you're older.

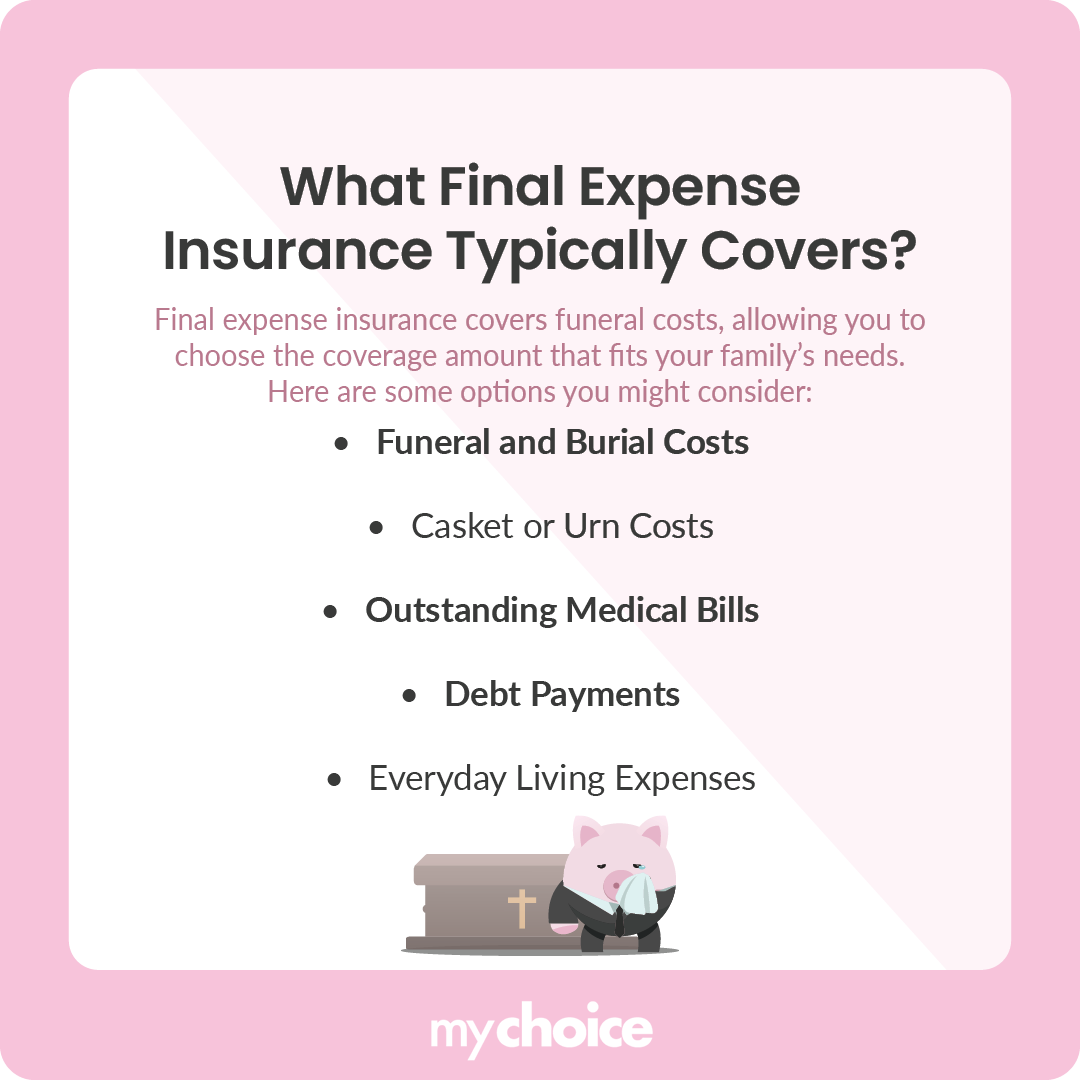

Final expenses are the expenditures your household spends for your funeral or cremation, and for various other things you may want during that time, like an event to celebrate your life. Although assuming concerning final expenses can be hard, knowing what they set you back and seeing to it you have a life insurance coverage policy huge adequate to cover them can aid save your household an expenditure they may not have the ability to pay for.

Which Is The Best Funeral Plan

One option is Funeral Preplanning Insurance policy which permits you choose funeral product or services, and fund them with the acquisition of an insurance coverage. An additional choice is Last Expense Insurance Policy. This sort of insurance policy supplies funds straight to your recipient to assist spend for funeral and various other expenses. The amount of your last expenses relies on numerous points, including where you live in the United States and what kind of final setups you want.

It is projected that in 2023, 34.5 percent of family members will certainly select burial and a greater percentage of households, 60.5 percent, will select cremation1. It's estimated that by 2045 81.4 percent of family members will certainly pick cremation2. One factor cremation is coming to be more prominent is that can be less costly than funeral.

Buy Final Expense Insurance

Depending upon what your or your household desire, things like burial stories, serious markers or headstones, and coffins can boost the rate. There may likewise be expenses in enhancement to the ones especially for interment or cremation. They could consist of: Treatment the price of traveling for household and enjoyed ones so they can go to a service Provided meals and various other expenses for a party of your life after the solution Purchase of unique attire for the service Once you have an excellent concept what your final costs will be, you can assist plan for them with the appropriate insurance plan.

Medicare only covers clinically needed costs that are required for the medical diagnosis and therapy of an illness or condition. Funeral expenses are not taken into consideration clinically essential and for that reason aren't covered by Medicare. Last expense insurance coverage provides an easy and relatively low-priced method to cover these costs, with plan benefits varying from $5,000 to $20,000 or even more.

Individuals generally acquire final expenditure insurance policy with the intent that the beneficiary will use it to pay for funeral costs, superior debts, probate costs, or various other relevant expenses. Funeral expenses might include the following: Individuals typically question if this sort of insurance coverage is necessary if they have cost savings or other life insurance policy.

Life insurance policy can take weeks or months to payment, while funeral expenses can start building up instantly. Although the beneficiary has the last word over exactly how the cash is utilized, these plans do make clear the insurance holder's intention that the funds be utilized for the funeral service and related prices. Individuals usually purchase long-term and term life insurance policy to assist offer funds for recurring expenditures after an individual dies.

Final Expense Life Insurance Policy

The very best way to guarantee the plan amount paid is spent where meant is to name a recipient (and, in some instances, a secondary and tertiary beneficiary) or to position your desires in a making it through will certainly and testament. It is frequently a good method to notify key recipients of their expected duties as soon as a Final Cost Insurance coverage is acquired.

Premiums start at $22 per month * for a $5,000 coverage plan (premiums will differ based on issue age, gender, and coverage amount). No clinical examination and no health inquiries are needed, and customers are ensured coverage via automatic certification.

Listed below you will certainly discover some frequently asked concerns ought to you pick to use for Last Expense Life Insurance Policy by yourself. Corebridge Direct certified life insurance coverage agents are waiting to respond to any type of added questions you may have regarding the security of your loved ones in the occasion of your passing.

The kid rider is purchased with the idea that your child's funeral expenditures will certainly be completely covered. Youngster insurance policy motorcyclists have a fatality advantage that varies from $5,000 to $25,000.

Funeral Plan Insurance Quotes

Note that this plan just covers your youngsters not your grandchildren. Last expense insurance plan benefits do not end when you sign up with a policy.

Motorcyclists consist of: Faster death benefitChild riderLong-term careTerm conversionWaiver of premium The increased death advantage is for those who are terminally ill. If you are seriously ill and, depending on your details policy, identified to live no longer than 6 months to two years.

The disadvantage is that it's going to reduce the fatality benefit for your recipients. The youngster rider is bought with the idea that your youngster's funeral service costs will be fully covered.

Coverage can last up until the kid turns 25. The long-term treatment rider is similar in principle to the sped up fatality advantage.

Best Final Expense

A person who has Alzheimer's and needs everyday aid from health and wellness aides. This is a living benefit. It can be borrowed against, which is really helpful because lasting care is a significant cost to cover. For instance, a year of having someone care for you in your home will cost you $52,624.

The motivation behind this is that you can make the button without being subject to a clinical test. And considering that you will certainly no longer get on the term plan, this additionally implies that you no more have to fret regarding outlasting your plan and shedding out on your fatality benefit.

Those with existing health conditions might encounter higher premiums or constraints on coverage. Keep in mind, policies normally cover out around $40,000.

Consider the monthly costs payments, but also the comfort and financial security it gives your family. For many, the confidence that their loved ones will certainly not be strained with financial hardship throughout a tough time makes last expenditure insurance coverage a worthwhile investment. There are two kinds of final expenditure insurance policy:: This type is best for people in relatively great health that are searching for a way to cover end-of-life prices.

Protection amounts for streamlined issue policies typically rise to $40,000.: This type is best for people whose age or wellness prevents them from getting other sorts of life insurance policy protection. There are no wellness requirements in any way with guaranteed issue plans, so anybody that satisfies the age needs can commonly certify.

Below are some of the variables you should take right into factor to consider: Review the application process for different plans. Make sure the service provider that you pick offers the quantity of protection that you're looking for.

{kind=link}

Latest Posts

Lenders That Accept Term Life Insurance As Collateral

What Is A Level Term Life Insurance Policy

Term Life Insurance Scam