All Categories

Featured

Simply select any kind of kind of level-premium, long-term life insurance coverage plan from Bankers Life, and we'll convert your plan without needing proof of insurability. Plans are exchangeable to age 70 or for 5 years, whichever comes later on - which of the following is characteristic of term life insurance?. Bankers Life uses a conversion credit rating(term conversion allocation )to policyholders up to age 60 and through the 61st month that the ReliaTerm policy has actually been in force

At Bankers Life, that means taking an individualized strategy to help safeguard the people and households we offer - what does level term life insurance mean. Our goal is to provide exceptional service to every policyholder and make your life much easier when it comes to your insurance claims.

Life insurance companies offer different kinds of term plans and conventional life policies as well as "rate of interest sensitive"items which have actually come to be a lot more prevalent because the 1980's. An economatic whole life plan gives for a fundamental quantity of taking part entire life insurance policy with an added supplementary coverage supplied through the usage of rewards. There are 4 basic rate of interest delicate entire life policies: The universal life plan is actually even more than rate of interest sensitive as it is made to reflect the insurance company's present death and expenditure as well as passion profits rather than historical rates.

You might be asked to make additional costs repayments where protection can end because the interest price dropped. The guaranteed price given for in the plan is much reduced (e.g., 4%).

Term Life Insurance For Spouse

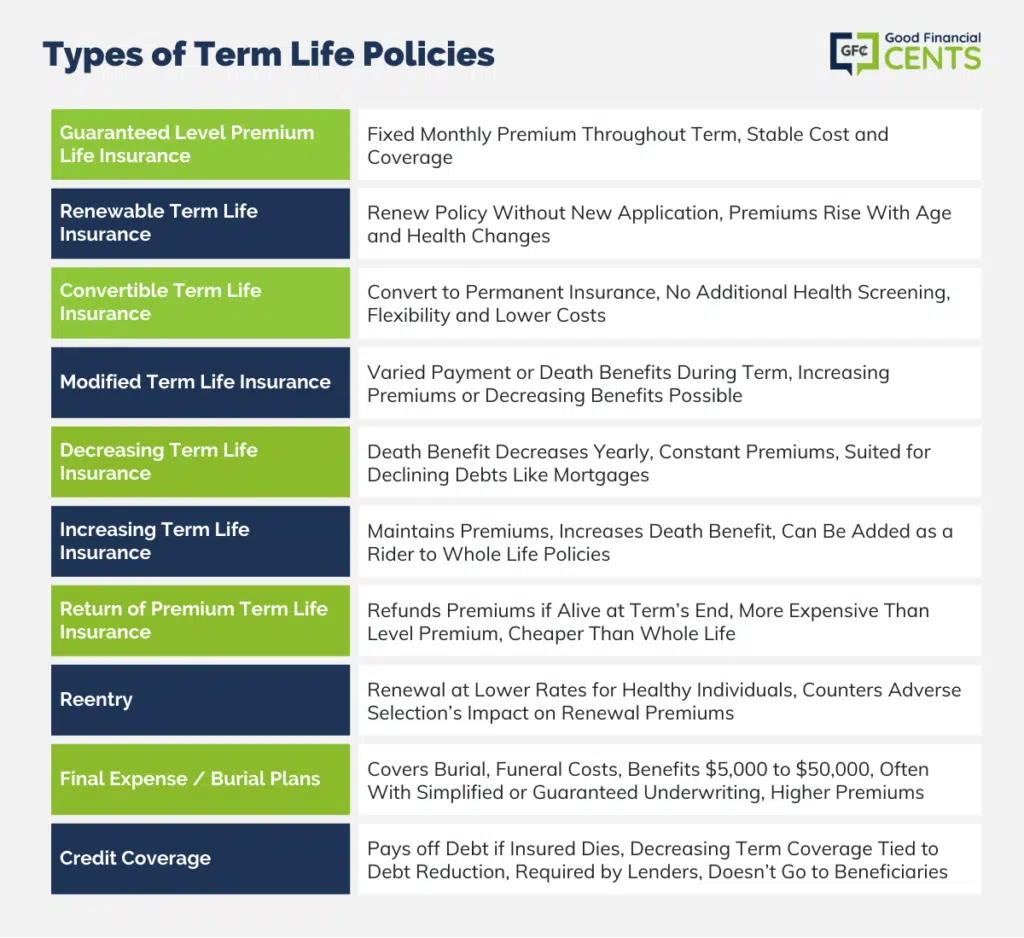

In either situation you must obtain a certificate of insurance policy explaining the arrangements of the team plan and any type of insurance policy charge. Typically the maximum quantity of protection is $220,000 for a mortgage and $55,000 for all various other financial debts. Credit report life insurance policy need not be bought from the organization providing the financing

If life insurance policy is needed by a creditor as a problem for making a loan, you might have the ability to appoint an existing life insurance coverage policy, if you have one. You may desire to acquire team debt life insurance in spite of its greater price since of its convenience and its accessibility, normally without in-depth proof of insurability. when term life insurance expires.

Nevertheless, home collections are not made and costs are mailed by you to the agent or to the company. There are certain factors that often tend to increase the costs of debit insurance greater than regular life insurance policy plans: Specific expenditures coincide regardless of what the size of the policy, to ensure that smaller sized plans provided as debit insurance will have greater costs per $1,000 of insurance policy than larger dimension regular insurance coverage

Because very early lapses are costly to a firm, the costs need to be passed on to all debit insurance policy holders. Because debit insurance policy is designed to consist of home collections, greater compensations and costs are paid on debit insurance than on routine insurance coverage. Oftentimes these higher expenses are passed on to the policyholder.

Where a firm has various premiums for debit and normal insurance policy it may be feasible for you to purchase a larger amount of regular insurance than debit at no additional expense - which of these is not an advantage of term life insurance. Consequently, if you are thinking about debit insurance, you should certainly examine normal life insurance policy as a cost-saving choice.

What Is A 10 Year Level Term Life Insurance

This plan is made for those who can not originally pay for the routine whole life costs however that desire the higher costs protection and feel they will at some point be able to pay the greater costs (when term life insurance expires). The household plan is a mix strategy that provides insurance policy defense under one agreement to all participants of your prompt family hubby, partner and children

Joint Life and Survivor Insurance policy gives insurance coverage for two or even more persons with the fatality advantage payable at the death of the last of the insureds. Premiums are dramatically lower under joint life and survivor insurance than for policies that guarantee just one individual, because the probability of needing to pay a death case is lower.

Premiums are significantly greater than for plans that insure a single person, because the probability of having to pay a fatality claim is higher (reduced paid up term life insurance). Endowment insurance policy attends to the payment of the face total up to your beneficiary if fatality takes place within a specific duration of time such as twenty years, or, if at the end of the particular duration you are still alive, for the repayment of the face total up to you

{kind=link}

Latest Posts

Lenders That Accept Term Life Insurance As Collateral

What Is A Level Term Life Insurance Policy

Term Life Insurance Scam